Our investment outlook for April 2025

The latest outlook from our specialists on 2025’s key investment themes

In our latest investment outlook, Thomas Becket, Co-Chief Investment Officer, reviews the first quarter of 2025, the evolving economic and geo-political landscape, and why there is still a strong case for investor optimism.

Theme 1: geopolitics, economics and monetary policy

‘Big wheels that keep on turning’

We live and invest in uncertain times – which won’t come as news to any of you.

At Canaccord Wealth, we like to describe the inconsistencies of geopolitics, economics and monetary policy as the ‘big wheels that keep on turning’. Those wheels sometimes rotate smoothly and in synchrony. At other times, they appear to crunch together, creating unpredictable jolts and friction. In more challenging times it can feel as if the wheels are falling off entirely.

Whether the wheels spin independently or rotate together matters for investors, but probably not as much as is generally assumed. In the last twenty years we have seen financial crises, economic downturns, periods of political chaos in Europe, geopolitical angst and outright war. We have also seen at least two significant equity bear markets and plenty of market corrections. However, during those two decades, investors have broadly been rewarded for making investments and sticking with them.

This is not to minimise the short-term volatility that grinding wheels can cause in financial markets. This can be worrying and unnerving for investors, but the long-term lesson learned is that it is a necessary part of any market cycle and can create opportunities, which investors can use to their advantage.

Theme 2: Market and investment volatility

How do we avoid the potholes?

We suspect that 2025 will continue to be a year of high drama, randomly spinning wheels and volatility. We are well prepared for this likelihood, which is reflected in our consistently balanced and diversified approach to investment. We believe investors should brace themselves for the skirmishes ahead and remember that the only real equation for future investment success is buying good investments at attractive valuations and holding them for a sensible period of time. Volatility across markets and in specific assets gives nimble investors an opportunity to fulfil this equation.

To say there is ‘a lot going on’ understates the oscillations that we are currently witnessing in geopolitics, politics and economics at the start of 2025: the early days and stated intentions of the Trump administration are driving significant change.

Theme 3: European economy

Getting ahead of steam – an economic boost

We might finally see some form of temporary ceasefire in Ukraine. A lasting peace would serve to cool the levels of tension globally. At the same time, the changing US-Europe relationship has forced European politicians out of their complacent slumber, spurring them to start increasing their defence spending. With the notable exception of Germany, there is no money available to ramp up this new required investment, so it will mean yet more debt, but it might provide an economic boost to the stagnant European economy.

Theme 4: Global supply chain

Fragmentation – or just grinding the gears?

Simultaneously, we are likely to see global supply chains become even more fragmented, with this expected to accelerate as Trump’s tariffs force trading partners to reconsider previously accepted trade policies and approaches. Trump has made it clear that he wants to reverse the decline in US manufacturing and production and will use tariffs as a means to achieve those aims. It may cause angst and upset many trading partners, but Trump is right to highlight this as an important societal and economic detractor to the US over the last few decades, and it was a key reason why he was elected.

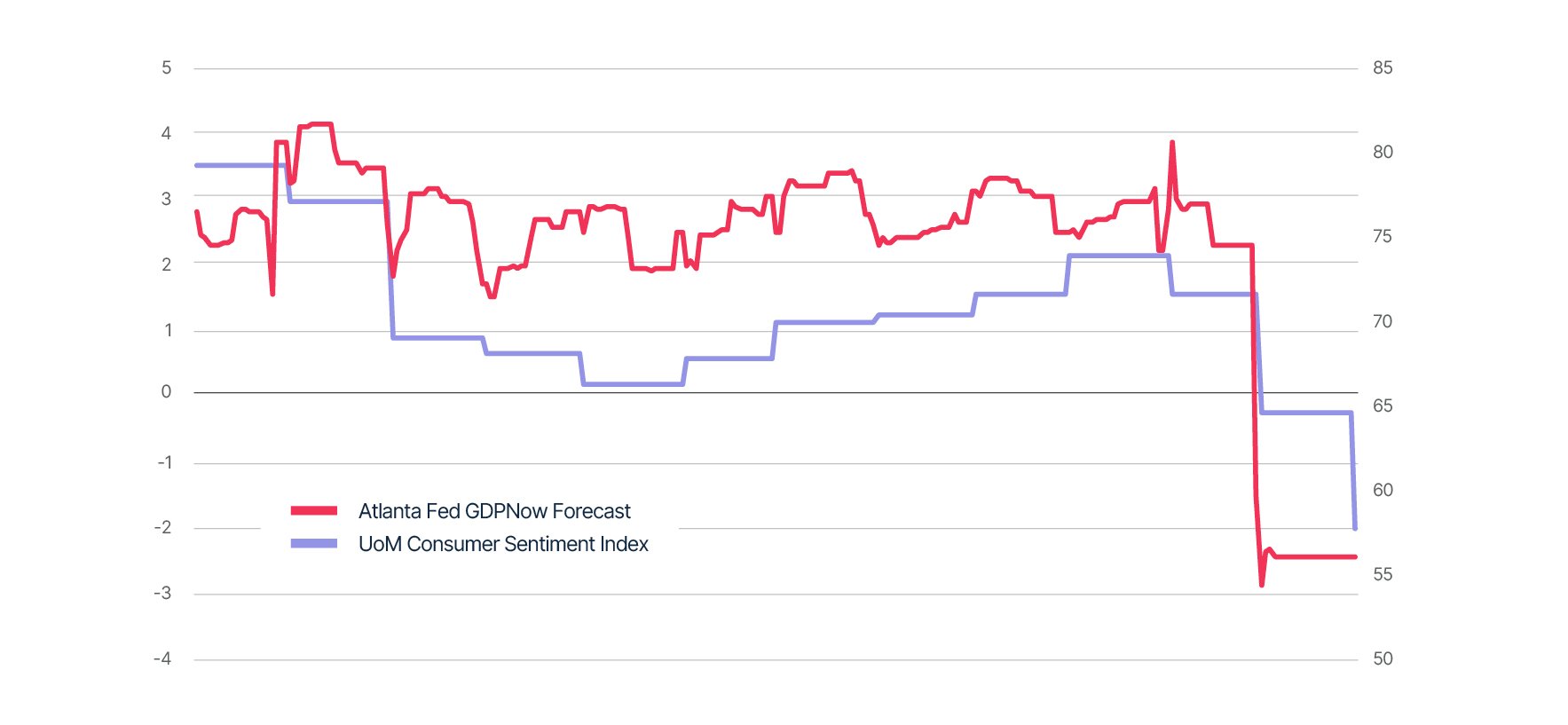

Notably, the unpredictable nature of Trump’s policies (even when he is simply enacting the promises of his successful election campaign) is creating economic uncertainty in the US. One of the big changes in early 2025 has been the start of an economic slowdown there as illustrated in fig 1 below. This has contributed towards the volatility seen across financial markets this year, but we do not believe this will be a particularly pernicious slump and it will be offset by more positive economic policies later in the year.

Theme 5: The US economy

Fig 1 Noise or signal: start of an economic slowdown in the US?

Source: Canaccord Wealth, Bloomberg – 01/04/2024 to 31/03/2025.

University of Michigan (UoM) Consumer Sentiment Index – a monthly survey measuring consumer confidence, a key economic indicator gauging consumer sentiment towards the economy and their financial situation.

The Atlanta Fed GDP Now forecast is a real-time model that provides an estimate of US GDP growth based on current economic data

We are also seeing a slightly better economic outlook in Europe, with plenty of fiscal support to come, as well as tentative signs of an improvement in China. We suspect that economic activity will remain low, but positive through the year, which should be sufficient to support asset markets.

There is also uncertainty over the path of inflation rates. Clearly, we are in a much better place than we were in 2022-2023, but the disinflationary progress has stalled in recent months and there is some evidence that inflationary pressures are percolating in the global economy once more. Economic distortions, increased defence spending and trade tariffs drive inflation uncertainty, which we view as a key risk for later in 2025 and we have mitigated against such a risk in our portfolios.

We suspect that the major central banks globally will be inclined to cut interest rates further as 2025 progresses: we anticipate two rate cuts in both the UK and the US this year. However, much will depend on how the economic picture and inflationary pressures unfold.

2025: making slow but steady progress

Our view at the start of the year was that portfolios would make positive progress again in 2025, building on the recovery that started in Autumn 2022. We expected both equities and fixed interest to deliver positive returns, assuming our expectations around the broad economic, inflation and interest rates were sensible.

At the same time, we expected the shape of returns to be different to those experienced in 2024, as there was a decent chance that we would start to see a broadening out of the gains globally, away from the US and technology towards Europe and defensive sectors. So far this has been the case, as sentiment towards the US has cooled from previously excessive optimism and hope of a better economic outlook for Europe has risen.

Finding the right way forward

With everything we have discussed in this edition of Outlook, as well as all the subjects we couldn’t find space for, it is obvious that an investor’s path through 2025 is a step into ‘The Great Unknown’. At the same time, there is much to be optimistic about rather than just much to fear.

We urge against excessive swings in sentiment and pursue a pragmatic approach. As long as we can continue to find sound investments – at appropriate valuations – we will remain confident, rather than complacent, about the prospects of positive outcomes from portfolios. Despite all those ‘big wheels turning’ at the moment, this remains very much the case today.

We are here to help

If you would like to discuss how your own portfolio is set up to navigate this outlook and still meet your long-term goals, please get in touch with your usual Canaccord account executive or email: questions@canaccord.com

For further information on any of the terms used in this article please see our glossary of investment terms.

The case for getting in the ring with UK equities

As we review the historic performance history of UK equities, we discuss why our client portfolios can still benefit from investing closer to home.

You may also be interested in:

New to Canaccord?

If you would like to know how we can help you to make the most of your wealth, contact one of our experts for a no-obligation, free consultation.

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested. Past performance is not a reliable indicator of future performance.

The information provided is not to be treated as specific advice. It has no regard for the specific investment objectives, financial situation or needs of any specific person or entity.

This is not a recommendation to invest or disinvest in any of the companies, themes or sectors mentioned. They are included for illustrative purposes only.

The information contained herein is based on materials and sources deemed to be reliable; however, Canaccord Wealth makes no representation or warranty, either express or implied, to the accuracy, completeness or reliability of this information. Canaccord Wealth is not liable for the content and accuracy of the opinions and information provided by external contributors. All stated opinions and estimates in this article are subject to change without notice and Canaccord Wealth is under no obligation to update the information.

Find this information useful? Share it with others...

Thomas Becket

A graduate of Trinity College, Dublin, with an MA (Hons) in Classics, Tom moved to Canaccord Genuity Wealth Management as part of the acquisition of Punter Southall Wealth, where he had been Chief Investment Officer for nearly 18 years. He is an Associate of the CISI and a respected commentator in the press, particularly on markets and economic matters.

Investment involves risk and you may not get back what you invest. It’s not suitable for everyone.

Investment involves risk and is not suitable for everyone.